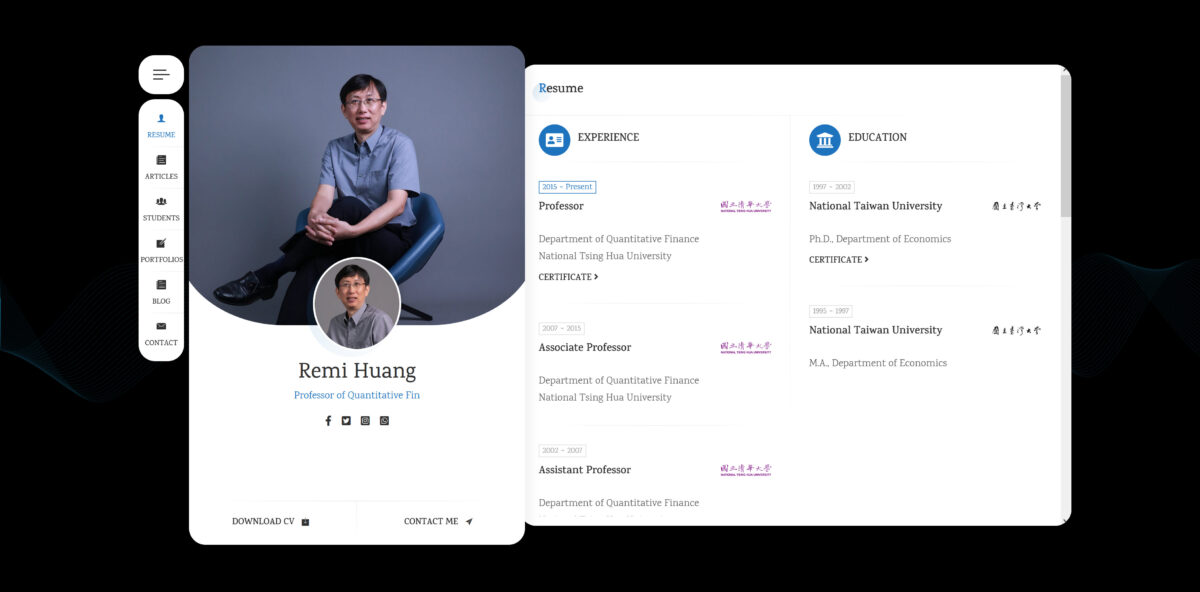

Department of Quantitative Finance

National Tsing Hua University

Professor of Quantitative Finance at NTHU

Researcher of CRETA at NTU

Professor of Quantitative Finance at NTHU

Researcher of CRETA at NTU

Department of Quantitative Finance

National Tsing Hua University

Department of Quantitative Finance

National Tsing Hua University

Department of Quantitative Finance

National Tsing Hua University

M.A., Department of Economics

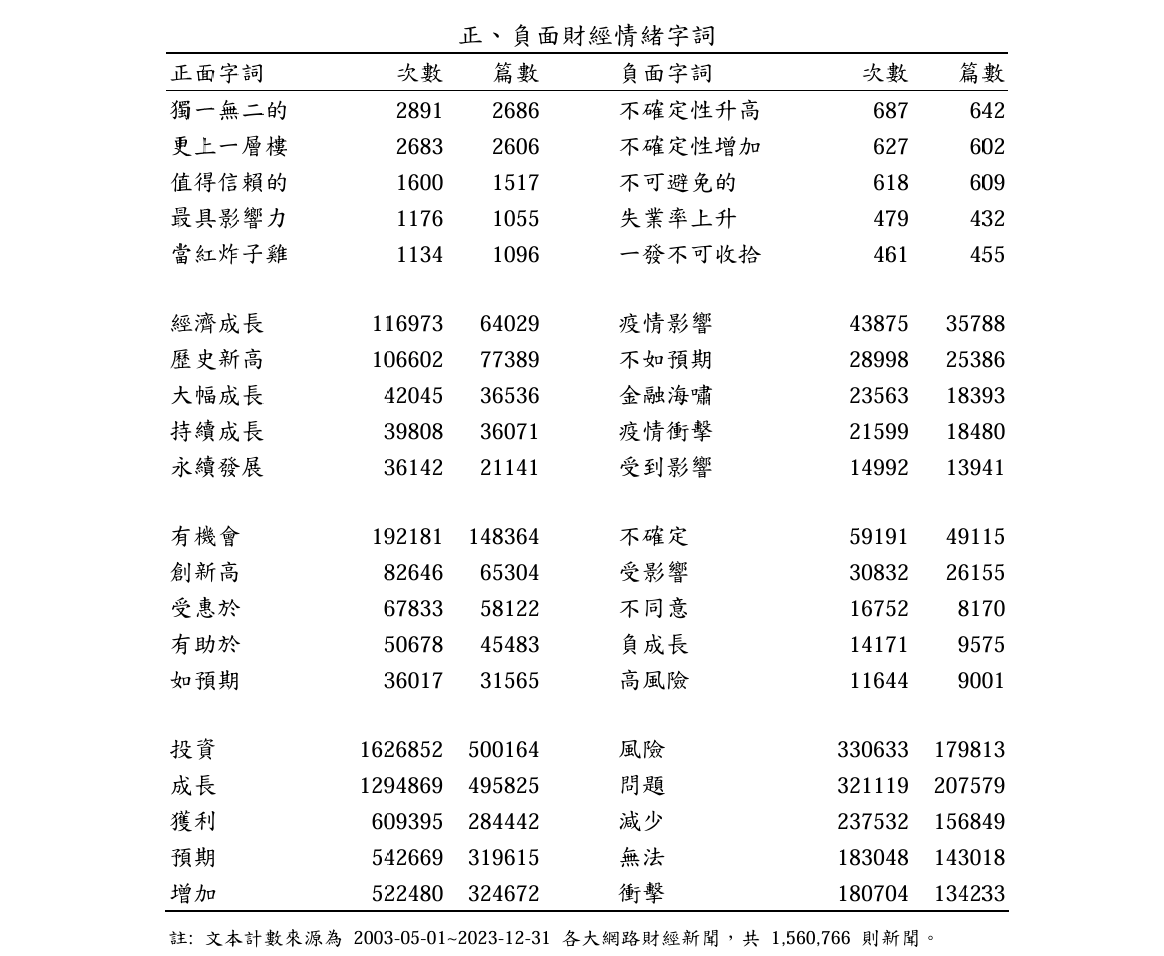

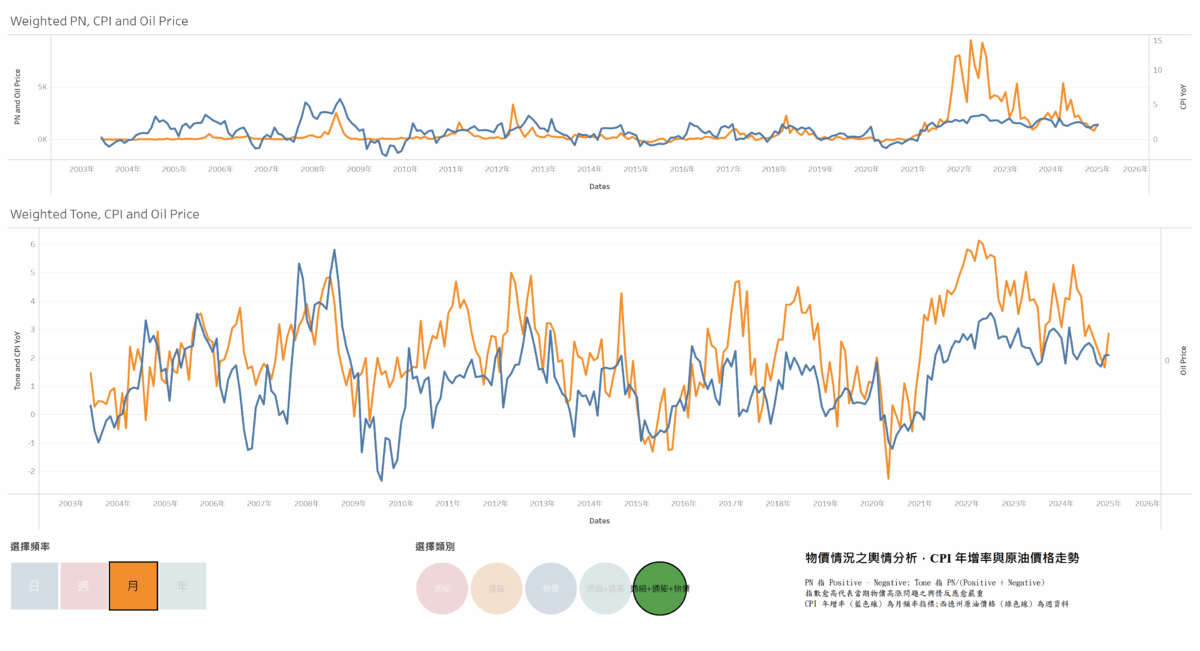

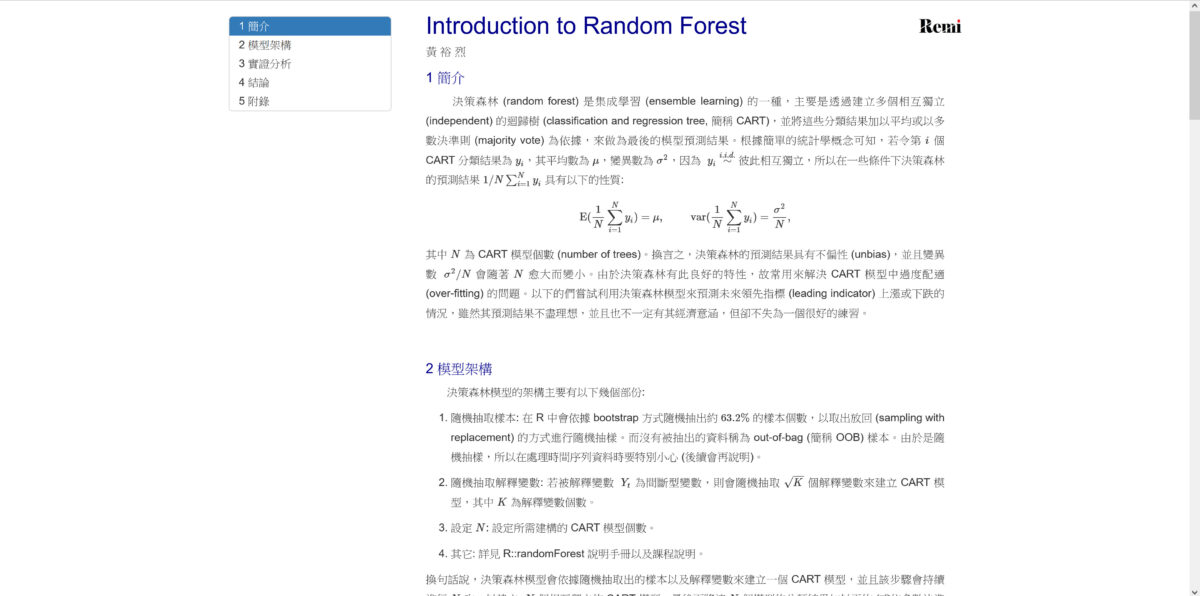

編製經濟指標的目的在於監測經濟狀況、預測未來趨勢、提供政策制定依據,並為市場決策與經濟評估提供參考。透過領先指標、房價指標、消費信心指標等數據,決策者、投資人和企業能夠掌握經濟變化,並據此調整策略。例如,以七項總體變數編製的領先指標可用來預測景氣循環,幫助政府制定適當的財政與貨幣政策;而透過大量房屋交易數據編製的房價指標則能反映房市熱度,影響購房與投資決策。此外,這些指標還可用於不同國家或區域間的經濟比較,進一步提升政策與市場決策的精確度。因此,經濟指標的編製不僅是衡量經濟表現的重要工具,也為決策者與市場參與者提供制定策略的關鍵依據。 編製經濟指標的方法很多,需依據不同應用場景選擇適當的計算方式。例如拉氏物價指數 (Laspeyres Price Index) 和帕氏物價指數 (Paasche Price Index) 便是常用的指數計算方式。拉氏指數以基期數量作為權重,計算較為簡單且適用於長期比較,但可能高估物價變動;帕氏指數則以現期數量為權重,能反映消費行為變化,但計算較為複雜,可能低估物價變動。因此,學者常採用費雪理想指數 (Fisher Ideal Index) 作為折衷方案,透過幾何平均方式綜合兩者優勢。此外,經濟學者也運用各種模型來編製指標,例如主成分分析 (如因子模型)、時間序列分析 (如 HP filter)、機器學習 (如 LSTM…

{kind=link}

{kind=link}